Is Economic Policy Ready for the Next Crisis?

At #LiNoEcon, three Nobel Laureates explored economists’ understanding of how policies on taxes, public spending and interest rates work together in a time of crisisAt #LiNoEcon, three Nobel Laureates explored economists’ understanding of how policies on taxes, public spending and interest rates work together in a time of crisis

#LiNoEcon Daily Recap – Friday, 25 August

Friday was the last day in Lindau but not the last day of the meeting. Saturday is going to take the #LiNoEcon participants to Mainau Island, so while you are enjoying your last day on the picturesque island, let’s take a look at what happened yesterday. Here are our highlights from Friday: Video of the day: […]

Winners and Losers From a ‘Commodities-For-Manufactures’ Trade Boom

#LiNoEcon participant Francisco Costa explores the effects of trade with China on Brazilian workers#LiNoEcon participant Francisco Costa explores the effects of trade with China on Brazilian workers

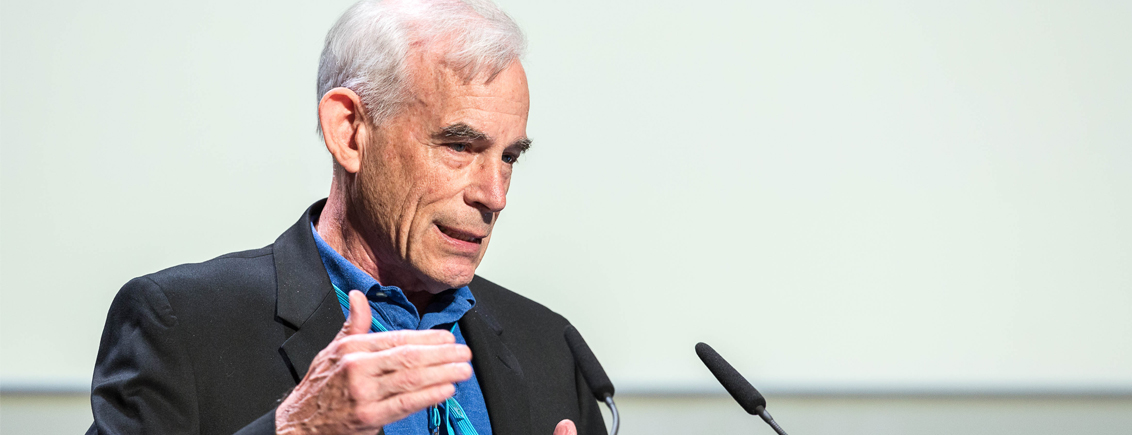

The Myth of the Independent Central Bank

Nobel Laureate Christopher Sims argues that since fiscal policy guarantees the value of fiat money, central banks can never be truly independent of governmentNobel Laureate Christopher Sims argues that since fiscal policy guarantees the value of fiat money, central banks can never be truly independent of government

The Puzzle of Global Inequality

At a Science Breakfast #LiNoEcon participants discussed fighting economic inequality through the food supply chainAt a Science Breakfast #LiNoEcon participants discussed fighting economic inequality through the food supply chain

#LiNoEcon Daily Recap – Thursday, 24 August

Thursday was packed with lectures, seminars and the first panel discussion of #LiNoEcon. In our mediatheque, you may find many great pictures, videos of exceptional lectures and thought-provoking blog contributions. There is so much more worth checking out than what we present to you in our daily recap, so do have a look. Enjoy the following […]

The Road to a Nobel Prize

Three recent Nobel Laureates in Economic Sciences discussed their work on contracts, incentives and organisations at #LiNoEconThree recent Nobel Laureates in Economic Sciences discussed their work on contracts, incentives and organisations at #LiNoEcon

‘Homo Economicus’ Reconsidered

Nobel economists rebel against simplistic conceptions of rationality at #LiNoEconNobel economists rebel against simplistic conceptions of rationality at #LiNoEcon

Warum Finanzminister CO2-Steuern befürworten

#LiNoEcon-Teilnehmer Max Franks erläutert, wie Klimaschutz und Investitionen in Infrastruktur miteinander vereinbar sind.#LiNoEcon-Teilnehmer Max Franks erläutert, wie Klimaschutz und Investitionen in Infrastruktur miteinander vereinbar sind.

Elderly Europe

Planning for the challenges of an ageing population requires international cooperation not competition, says Frances CoppolaPlanning for the challenges of an ageing population requires international cooperation not competition, says Frances Coppola

Housing Talk: Why You Should Never Trust a House Price Index (Only)

#LiNoEcon participant Sofie Waltl on the dangers of booming markets for property#LiNoEcon participant Sofie Waltl on the dangers of booming markets for property

#LiNoEcon Daily Recap – Wednesday, 23 August

On Wednesday, #LiNoEcon was inaugurated with a keynote by ECB President Mario Draghi, followed by the first full day of the meeting programme with lectures and seminars. In the evening, young economists and laureates mingled at the Get-Together in Friedrichshafen, where Federal Minister Peter Altmaier welcomed the participants on behalf of the German government, stressing […]